The simple secret to building a multi-property portfolio

If you want to build substantial wealth through property, there’s one easy formula you need to understand.

Blogger: Cam McLellan, director, OpenCorp

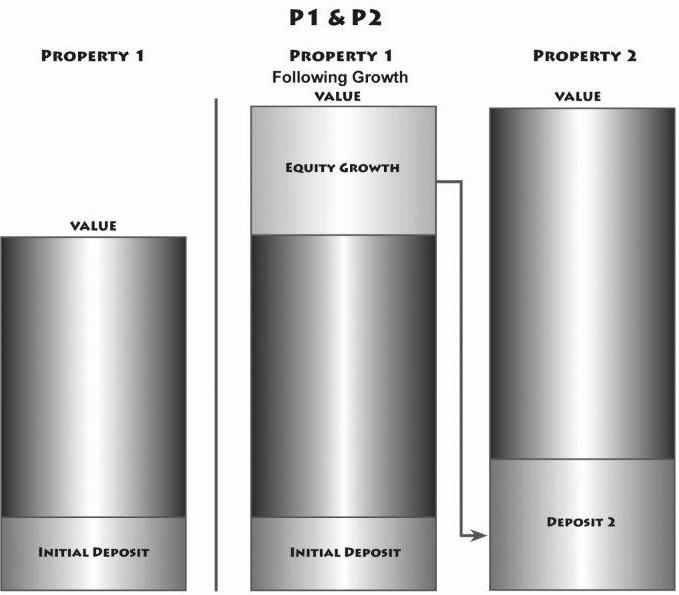

The key to building a strong portfolio is identifying that your usable equity has increased. Banks will convert this usable equity into cash, which can be used for deposits on further investments.

This is called duplication.

“Why is it important to understand duplication?”

Duplicating an effective investment system is the important thing. If you learn to continually buy good investments, duplication is fantastic. Duplication without a system only compounds risk.

The key to duplication is to have a system that ensures that you regularly monitor any market price movement. When a lift in price is identified, revalue your portfolio, increase your line of credit (or “contingent liability”) and unlock usable equity and duplicate.

The common term for having usable equity just sitting doing nothing is lazy equity. If you’re growing your property portfolio, then having lazy equity is one of the biggest and most common mistakes you can make.

“How can equity be called ‘lazy’?”

Lazy equity is the term for equity you have at your disposal that is sitting idle doing nothing. To supercharge your investment strategy, use available equity for the deposits on additional investments.

Every day that passes when you have lazy equity sitting idle means you are missing out on opportunities to duplicate and move closer to financial freedom.

I have included a simple diagram titled “P1 buys P2” that shows how to duplicate your portfolio by utilising the increase in usable equity from one property to purchase another. This means that you don’t have to save for each deposit. Imagine when you have several properties and they all go through a growth cycle. The large increase in equity means your ability to duplicate compounds.

Next I have outlined a very conservative scenario that shows what is achievable through duplication.

The core theory of duplication has been around for centuries. Sadly, there are people in the investment world today who would have you believe they themselves created this basic system. No person alive can take credit for this. Duplication has been around since the first time someone planted an apple seed.

The more property value you hold in your portfolio when a price rise occurs, the more usable equity you create and therefore the more substantial the equity platform you have to duplicate further from. This is called the compounding effect. You will notice the compounding effect once you have multiple properties that go through a growth period. When this happens, let the good times roll.

The key is to enter the market as soon as possible, then duplicate each time as soon as you have usable equity. (While you invest your equity in your investments, ensure that you invest your time in education. Investment knowledge will help you to avoid costly mistakes.) According to the Australian Taxation Office (ATO) only 15,483 people in Australia own more than six properties. That means the people who do own more than six properties essentially own a lot more than six properties. This means the rich are still getting richer and everyone else is still doing the same old thing. The good thing is that investing is not that hard once you’ve started.

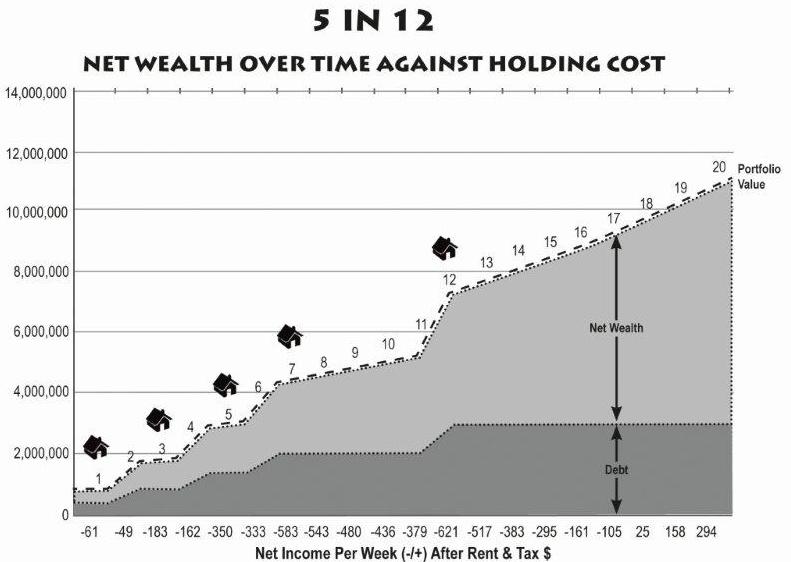

Now, let’s look at a safe example of what’s achievable. I want to illustrate to you that you don’t have to own an entire city suburb to achieve financial independence. In reality, a handful of smart investments are all that are required. I have outlined this for you in a scenario; five very conservative properties purchased over a 12-year period. I have then shown the growth that occurs up to the 20-year mark, even if you were to stop acquiring additional properties at the 12-year mark.

I have used some standard assumptions that are factored evenly each year. Please understand that things like capital growth, rental yield and wage increases never increase evenly each year. Over a longer period, such as 10 or 20 years, I’d still expect some variance, but the examples below are reasonable assumptions to use for this exercise.

For this example, I have used a wage of $90k per annum (the average household income).

Factored is a 5 per cent wage increase per year.

First property purchased at $400,000.

An increase of 8 per cent in property value per year.

Rental yield of 4.5 per cent of the property’s value.

Interest rate of 7 per cent.

I want you to understand something when you are building wealth. It’s not all about the amount of individual properties you accumulate; it’s the net wealth that’s built over time that really matters. I have specifically made this example very conservative – five properties purchased over 12 years – to show that real wealth is achievable at a very safe level.

You will notice in the chart 5 IN 12 that it illustrates several things. First the year that each of the five properties are purchased, the portfolio’s total value, the net wealth, as well as debt that accumulates and also the weekly holding costs. For the first five or six years, things build slowly, but as growth occurs while holding a reasonable asset base, your wealth compounds and starts to climb at a much faster rate. You will also notice that the debt level remains the same after year 12, which is when the final property has been acquired.

I have noted against each year along the bottom of the 5 IN 12 chart the weekly holding costs after rent and tax. I haven’t sugar-coated these figures. You may note that the weekly holding costs around years 11 to 13 may seem hard to sustain on the basic household wage. The holding costs at this point are at their peak, about $100 per week, per property. That’s around $32k per year net, after tax. Now that’s a very large amount of money if you were to use your earned income to cover the holding costs.

Never fear. What you will also notice is that during these years the net wealth is increasing, on “average” at a much faster rate per year than the holding costs. What I recommend is that you access this equity to cover your holding costs; you will do this by refinancing and creating a line of credit. For a period you’ll need to use these funds until the rent increases to the point that it will cover the holding costs of your portfolio. This is standard practice for anyone building a portfolio.

Also, by having this line of credit available, you are able to cover any loss of income for the weeks between tenants and any repairs that may be needed. This way, along your investment journey, you will still be able to live a reasonable lifestyle while building your wealth. Remember, this equity is to be used for holding costs or future deposits, not toys.

What is important to focus on is the level of net wealth achieved by year 15. You may seem amazed by the results, but as Einstein said in reference to the compounding effect:

“Compounding is the eighth wonder of the world. He who understands it, earns it ... he who doesn’t pays it.”

The amount of net wealth at year 15 will be in the vicinity of $5.9 million and the portfolio’s total value will be around $8.5 million. If you factor growth of 8 per cent on your $8.5 million portfolio value (growth of 8 per cent on $8.5 million is about $680k per annum) you are now simply able to live off the equity growth on your property portfolio. This is why an equity growth strategy will always smash an initial positive cash flow strategy.

You will never save your way to wealth from a wage or rental income.

As mentioned, it’s important to understand that growth won’t occur evenly each year, but once you do experience a growth period while holding a number of properties, working for a living at this point becomes a choice!

Five properties in 12 years is a very conservative approach to investment. But I want you to understand that these five well-chosen properties are all that are required to give you a very comfortable lifestyle.

Another very achievable aim is to build a portfolio of 10 properties in 10 years. I’ve seen many people achieve this, but this does require a larger personal income to assist with the portfolio’s initial holding costs.

The key is to build momentum so that by year eight, nine and 10 you can buy two properties a year. It may sound hard, but when you have, for example, four properties that all have an increase in value, picking up an extra two or more at a time after that is very easy. You may find you purchase one property in the first year then none for a couple of years. You’ll then find that you might purchase two, three or more properties in a single year.

To achieve this you must follow a system that allows you to accurately monitor the market price on a regular basis. Checks every three months are ideal; six months worst case. Once you achieve a gain in usable equity, the key is to act quickly and purchase again. Then, once you’ve purchased all the properties possible using your usable equity, sit back, enjoy life and wait for a market rise to occur again.

Tips

• Banks will convert usable equity into cash, which can be used for deposits on further investments. This is called duplication.

• Usable equity just sitting doing nothing is called lazy equity.

• The more property value you hold in your portfolio when a rise occurs, the more usable equity you create and therefore the more substantial the equity platform you have to duplicate further from. This is called the compounding effect.

• The key is to enter the market as soon as possible then duplicate each time, as soon as you have enough usable equity.

Want to see more stories from trusted news sources?

Make Smart Property Investment a preferred news source on Google.

Click here to add Smart Property Investment as a preferred news source.